Interesting stats, suggesting that the underground economy is not currently growing in Canada. The CRA is careful to say that the UE is not an estimate of the tax gap, but CRA will look at these stats in light of the need to ensure everyone is "paying a fair share." I'm only aware of an official statement of a "tax gap" by the U.S. and U.K.

Sunday, September 30, 2012

Friday, September 28, 2012

Carter Commission after 50 years, cont'd

Today's panels were interesting and informative. Neil Brooks kicked things off with a lively and wonderful introduction to the politics and process of the commission and the hopes for tax reflection and reform today (they are dismal, I'm afraid). Tomorrow promises to be equally full, with a deep lineup. Speakers:

- Jinyan Li - Would Mr. Carter be Happy with the International Tax Developments in Canada

- Yan Xu - Enduring Echoes in a Changing Landscape: China’s Tax History?

- Carl MacArthur - From Carter to Copthorne: Judicial Inactivism and the Rise of the GAAR

- Michelle Markham - Advance Pricing Arrangement Reform in Australia – Is this Relevant to any Future Reform in Canada?

- Kathrin Bain - Research and Development Tax Incentives: What can Canada learn from Australia’s experiences?

- Steven Dean - Tax Apps: 50 Years of Tax Expenditures

- Lisa Philipps - The Role of R&D Tax Expenditures in Canada’s Innovation Strategy: From Carter to Jenkins

- Michael Livingston - Convergence, Divergence, and the Limits of Globalization in Tax Matters: The Canadian Experience

- William McCarten - Provincial Strategies for Corporate and Personal Income Tax Design: Positive, Zero, or negative Sum Games?

- Kathryn James - The Carter Commission and the Value Added Tax

- Lori McMillan - The Non-charitable Non-profit Subsector in Canada: An Empirical Examination

- Richard Schmalbeck - The Income Taxability of Gifts: Haig-Simons, the Carter Commission, and the Real World

- Shu Yi Oei - Who Wins When Uncle Sam Loses? Social Insurance and the Forgiveness of Tax Debts

- Catherine Brown - Revisiting the Carter Commission's International Tax Policy Analysis

- Elsbeth Heaman - The Personal Income Tax in Canada Before 1917

- David Tough - Carter and Company: The Commission’s Critique of Inequality in the Context of Canada’s Rediscovery of Poverty in the 60s

- Neil Buchanan - The Trinity without the Holy Ghost: Tax Scholarship Without the Illusory Goal of Efficiency

- David Duff - Haig, Simons, and Carter: Rethinking the Concept of Income in Tax Law and Policy

- Richard Krever - What is an “Enterprise” in GST Law?

- Shirley Tillotson - The Politics of Carter-Era Tax Reform: A Revisionist Account

Thursday, September 27, 2012

Carter Commission After 50 Years

Tomorrow is the first day of the Dalhousie Law conference, The Carter Commission 50 Years Later: A time for reflection and reform." On the schedule for tomorrow:

Neil Brooks - The Carter Report: Brilliant, Imaginative and One of a Kind

Ajay Mehrotra - The VAT Laggards: A Comparative History of US and Canadian Resistance to the Value-Added Tax

Miranda Stewart - Tax Reform and Legitimacy in the Global Era

Faye Woodman - Should the Tax Burden on Babyboomers Be Reduced Because They are Getting Older?: The Age Tax Credit, the Pension Income Credit, and Income Splitting of Pension Income

Claire Young - Beyond Conjugality: Time for the Tax System to Take that Concept Seriously

Allison Christians - Drawing the Boundaries of Tax Justice

Peter Dietsch - Fiscal Obligations to Redistribute in an International Setting

Thaddeus Hwong - A Comparison of Trends in Tax Levels and Tax Mixes in Canada and Other OECD Countries Before and After Carter

Chris Sprysak - Taxing Me or We: Yet Another Look at the Carter Commission’s Recommendation for Joint Returns

Tamara Larre - Dependency Under Canada’s Income Tax System

Kirk Collins - Capital Markets, Interest Imputation, and the Carter Report’s Proposed System of Full Integration of the Corporate-Shareholder Income Taxes

Martha O’Brien - Corporate Group Taxation: Here and Now, There and Then

And that's just the first day. You can access the full schedule at the link.

Wednesday, September 26, 2012

Today at McGill Law: Miranda Stewart

Miranda Stewart will present a paper on the sham doctrine today as the first speaker of the McGill Tax Policy Colloquium. It's an interesting paper that raises difficult questions about form and substance in tax law. If you're in Montreal, I invite you to attend, details at the link.

Tuesday, September 25, 2012

Why does Apple have so much cash offshore?

And Google and GE and etc etc? Contrary to popular sentiment, it is not that pesky uncompetitive U.S. tax regime, with its punitive rules that would impose corporate taxes on repatriated cash. At least, there is not enough empirical evidence to pin solely on this well-worn scapegoat. Instead, three economists examined the evidence of the growing MNC overseas cash stash and conclude that rather than regulation or governance, a company's spending on research and development intensity explains its cash overseas.

Defining as normal cash holdings the holdings a firm with the same characteristics would have had in the late 1990s, we find that the abnormal cash holdings of U.S. firms after the crisis represent on average 1.86% of assets. While U.S. firms held less cash than comparable foreign firms in the late 1990s, by 2010 they hold more. However, only U.S. multinational firms experience an increase in abnormal cash holdings during the 2000s. U.S. multinational firms had cash holdings similar to those of purely domestic firms in the late 1990s, but they hold over 3% more assets in cash than comparable purely domestic firms after the crisis. Further, U.S. multinationals increased their cash holdings since the late 1990s relative to foreign multinationals by roughly the same percentage as they increased their cash holdings relative to U.S. domestic firms. A detailed analysis shows that the increase in cash holdings of multinational firms cannot be explained by the tax treatment of profit repatriations, that it is intrinsically linked to their R&D intensity, and that firms that become multinational do not increase their abnormal cash holdings after they become multinational. There is no evidence that poor investment opportunities, regulation, or poor governance can explain the abnormal cash holdings of U.S. firms after the crisis.

U.S. firms hold more cash than comparable firms whether these firms are in developed countries or not, in common law countries or not, in countries that tax income worldwide or not, and in Eurozone countries or not.

...We find that U.S. multinationals held comparable amounts of cash than purely domestic firms in the late 1990s, but now hold significantly more cash than similar purely domestic firms.

...Foley, Hartzell, Titman, and Twite (2007) show that the tax treatment of remittances makes it advantageous for multinationals to keep their earnings abroad and they find that firms for which repatriation is more costly hold more cash. Our findings suggest that the tax costs of repatriation are not the whole story for the increase in cash holdings of U.S. multinationals in the 2000s. ...[T]he Homeland Investment Act of 2004 ... failed to reduce the cash holdings of multinational firms. ...[I]t could be that the incentives of the Act were insufficient to affect firms’ cash holdings. ...[T]he repatriation tax costs could affect more where firms locate their cash rather than how much cash they hold. We expect that the tax cost of repatriation would be more important for high cash flow multinationals, but empirically these multinationals do not hold more cash than low cash flow multinationals. The increase in cash holdings of multinationals is strongly related to their R&D intensity, so that multinationals with no R&D expenditures do not have an increase in abnormal cash holdings compared to domestic firms with no R&D expenditures. Further, a striking result is that, among high R&D spending firms, firms that were already multinationals before 1998 do not hold more cash now than firms that were purely domestic firms before 1998. Among these firms, cash holdings increase sharply for multinationals relative to purely domestic firms, but that is because the cash holdings of multinationals are becoming more comparable to the cash holdings of purely domestic firms. Finally, and perhaps most importantly, we find no evidence that firms that become multinationals start holding more cash after they become multinationals. It appears that firms that become multinationals are firms with attributes that lead them to hold large amounts of abnormal cash even before they become multinationals.Emphases mine.

An emergency room is not a health care plan.

American College of Emergency Physicians (ACEP):

"Emergency departments have become a health care safety net for everyone, but that safety net is breaking. If you continue to take emergency care for granted, and don’t support it, it eventually won’t be there for anyone.”So, it's not a vey good hammock then, either. It seems sad to me that the ACEP has to explain why emergency room care is not health care. An ounce of prevention is worth a pound of cure. That's a conservative (small c, obviously) idea. Yes, both cost money. One you plan for, and it costs x. The other you don't plan for and it costs x+. Not having national health care doesn't get everyone out at zero. I would rather pay for everyone at x instead of everyone at x+.

Monday, September 24, 2012

US to Europe: our airlines won't obey your tax laws

The EU is trying to take the high road on pollution, but the US insists on the low road:

In the meantime, I'm not sure I understand how the U.S. can simply declare that its airline industry can ignore the law in Europe.

The Senate unanimously passed a bill on Saturday that would shield U.S. airlines from paying for their carbon emissions on European flights, pressuring the European Union to back down from applying its emissions law to foreign carriers.

...Republican Senator John Thune, a sponsor of the measure, said it sent a "strong message" to the EU that it cannot impose taxes on the United States.The aviation industry is happy of course; as the EU was already considering backing down, "to avert a trade war with major economic powers such as China and the United States, allowing time to forge a global agreement on climate charges for the aviation industry." But that's waiting for Godot: "attempts to address this problem on a global basis have been festering for more than 15 years in ICAO and the United States is at the centre of the problem," according to Transport & Environment, an NGO based in Brussels.

In the meantime, I'm not sure I understand how the U.S. can simply declare that its airline industry can ignore the law in Europe.

Who built that: fracking edition

Love it or hate it, fracking is not the product of private enterprise alone but a partnership between government and private enterprise, as the AP reports:

I'd like my money back, please.

Over three decades, from the shale fields of Texas and Wyoming to the Marcellus in the Northeast, the federal government contributed more than $100 million in research to develop fracking, and billions more in tax breaks. Now, those industry pioneers say their own effort shows that the government should back research into future sources of energy — for decades, if need be — to promote breakthroughs.

...The first federal energy subsidies began in 1916, and until the 1970s they "focused almost exclusively on increasing the production of domestic oil and natural gas," according to the Congressional Budget Office.

More recently, the natural gas and petroleum industries altogether accounted for about $2.8 billion in federal energy subsidies in the 2010 fiscal year and about $14.7 billion went to renewable energies, the Department of Energy found. The figures include both direct expenditures and tax credits.

Congress passed a huge tax break in 1980 specifically to encourage unconventional natural gas drilling, noted Alex Trembath, a researcher at the Breakthrough Institute, a California nonprofit that supports new ways of thinking about energy and the environment. Trembath said that the Department of Energy invested about $137 million in gas research over three decades, and that the federal tax credit for drillers amounted to $10 billion between 1980 and 2002.More at the link. Too bad all that subsidy has produced a process that sets your water on fire.

I'd like my money back, please.

A message to lobbyists in the pulpit: free speech does not mean tax-exempt speech.

The headline is "More than 1,000 pastors plan to challenge IRS by endorsing presidential candidate." The case for revocation of federal tax-exemption in these cases is 100% clear. The U.S. tax code exempts charitable organizations from federal taxation so long as they are not engaged in lobbying:

Corporations ... organized and operated exclusively for religious, charitable ...[etc] purposes ... no substantial part of the activities of which is carrying on propaganda, or otherwise attempting, to influence legislation ... and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office [shall be exempt from taxation under this subtitle]. 26 U.S.C. 501(c)(3).That's the U.S. Code, written by the Congress and enacted through legislative process into law. Not some whimsical action by the IRS, an agency of the federal government. Yet the leader of the campaign tries to make this about suppression of free speech by the IRS:

The purpose is to make sure that the pastor — and not the IRS — decides what is said from the pulpit,” Erik Stanley, senior legal counsel for the group, told FoxNews.com. " “It is a head-on constitutional challenge.”This is plain and simple a fabrication. There is no constitutional challenge here because there is no denial of free speech here. The IRS does not tell you what you can or can't say from the pulpit, any more than it tells you what you can or can't say anywhere else. Rather, the IRS is supposed to enforce the law as written. As far as the code goes, it is a pretty clear rule. You can say whatever you want but the fed does not have to pay you for it. So the right result here is revocation of exemption status.

Thursday, September 20, 2012

Tax transparency in Canada-report

I recently posted my Canadian National Report prepared for the Vienna University of Economics and Business, Conference on tax secrecy and transparency, Rust, Austria, July, 2012. From the abstract:

The aim of the project is to assess how different countries regard the treatment of tax information and tax secrecy. Topics include the collection of data, the sharing of information domestically and internationally, interaction of tax rules with related regulatory rules, and access to taxpayer information by the public. This report discusses Canada's relatively low profile in the global market for offshore financial services. Overall, Canada’s tax regime attempts to strike a balance between protecting taxpayer rights to privacy and confidentiality, and ensuring that the government has sufficient information about taxpayers in order to enforce its own laws, as well as to cooperate with efforts by other countries to enforce their tax laws in respect of their residents who invest in Canada.I invite you to download the paper from SSRN here. (link fixed, i think)

Latest on Vodafone in India

Vodafone is setting aside some pretty big numbers, notwithstanding the Economist's characterization of the rules as delayed and diluted.

What can you do with a shell company?

NPR's Planet Money has a new podcast that is a must listen:

A few months back, we set up a couple shell companies — Unbeliezable, Inc., in Belize, and Delawho? in Delaware.

On today's show, we talk to some tax lawyers to try to figure out what we can do with our companies. We draft a resolution so we can go to Belize to meet the fake director and fake shareholder of our company. And we learn owning shell companies in tax havens is a lot more of a hassle than we thought.

Wednesday, September 19, 2012

What's So Wrong with the St. Kitts & Nevis Investor Citizenship Plan?

Allison recently blogged about a plan from St. Kitts & Nevis to grant citizenship to investors in a hotel recently opened there. This is seen by some as a fundamental threat to democracy, sovereignty, and all other forms of good things. Apparently, the reason is supposed to be self-evident. Unfortunately, I am having trouble seeing it.

For decades, countries have been told that the problem with tax havens is that income is allocated to them with no "real" corresponding economic activity. Proposals to fight this have included punishments for taxpayers who invest in countries without "real" economic activity and a shift from transfer pricing to formulary apportionment based on "real" economic factors such as sales. The theme seemed pretty clear - real economic activity is necessary to apply tax laws.

So St. Kitts & Nevis found a way to build a real hotel really located in the real country. Isn't this exactly what all these people wanted?

Perhaps what bothers some is the appearance that a state seemingly "sold" its citizenship, and that states should not use their sovereign powers for such crass ends as private economic gains. But how is this any different than the state of Connecticut using its sovereign eminent domain power to take land away from poor, local residents and give it to a wealthy out-of-state private corporation? There is no doubt (at least according to the Supreme Court) that this is just fine - so how is it any different from what St. Kitts & Nevis is doing?

Similarly, the United States has no problem granting citizenship to engineers or other high-skilled people (including its own investor visa program), while it denies citizenship to poor migrant workers. What's the difference? Should St. Kitts & Nevis only be allowed to grant citizenship to poor, unskilled people and leave the wealthy and skilled to countries such as the United States and United Kingdom?

If a real hotel, really located, and really operating in St Kitts & Nevis is not sufficient to allow St Kitts & Nevis to impose its laws on the hotel's investors (whether good and bad), it is difficult to think of what would be. Perhaps that is the real threat to sovereignty and democracy.

For decades, countries have been told that the problem with tax havens is that income is allocated to them with no "real" corresponding economic activity. Proposals to fight this have included punishments for taxpayers who invest in countries without "real" economic activity and a shift from transfer pricing to formulary apportionment based on "real" economic factors such as sales. The theme seemed pretty clear - real economic activity is necessary to apply tax laws.

So St. Kitts & Nevis found a way to build a real hotel really located in the real country. Isn't this exactly what all these people wanted?

Perhaps what bothers some is the appearance that a state seemingly "sold" its citizenship, and that states should not use their sovereign powers for such crass ends as private economic gains. But how is this any different than the state of Connecticut using its sovereign eminent domain power to take land away from poor, local residents and give it to a wealthy out-of-state private corporation? There is no doubt (at least according to the Supreme Court) that this is just fine - so how is it any different from what St. Kitts & Nevis is doing?

Similarly, the United States has no problem granting citizenship to engineers or other high-skilled people (including its own investor visa program), while it denies citizenship to poor migrant workers. What's the difference? Should St. Kitts & Nevis only be allowed to grant citizenship to poor, unskilled people and leave the wealthy and skilled to countries such as the United States and United Kingdom?

If a real hotel, really located, and really operating in St Kitts & Nevis is not sufficient to allow St Kitts & Nevis to impose its laws on the hotel's investors (whether good and bad), it is difficult to think of what would be. Perhaps that is the real threat to sovereignty and democracy.

Tuesday, September 18, 2012

Private vs Public Healthcare Systems

Here is an interesting paper on private vs public health care systems in low- and middle-income countries, published earlier this year in PLOS Medicine, an open-access medical journal, in which the authors find that private systems don't deliver better efficiency, accountability or medical effectiveness in comparison to public systems. But they might be faster and nicer to you in a private care system. From the paper:

Introduction

Private sector healthcare delivery in low- and middle-income countries is sometimes argued to be more efficient, accountable, and sustainable than public sector delivery. Conversely, the public sector is often regarded as providing more equitable and evidence-based care. We performed a systematic review of research studies investigating the performance of private and public sector delivery in low- and middle-income countries.

Methods and Findings

...Comparative cohort and cross-sectional studies suggested that providers in the private sector more frequently violated medical standards of practice and had poorer patient outcomes, but had greater reported timeliness and hospitality to patients. Reported efficiency tended to be lower in the private than in the public sector, resulting in part from perverse incentives for unnecessary testing and treatment. Public sector services experienced more limited availability of equipment, medications, and trained healthcare workers. When the definition of “private sector” included unlicensed and uncertified providers such as drug shop owners, most patients appeared to access care in the private sector; however, when unlicensed healthcare providers were excluded from the analysis, the majority of people accessed public sector care. “Competitive dynamics” for funding appeared between the two sectors, such that public funds and personnel were redirected to private sector development, followed by reductions in public sector service budgets and staff.

ConclusionsThe incentive structure is interesting and echoes thoughts I've had before on privatizing water and waste disposal. This study is not about high income countries, but the health care cost difference between the US and the rest of the high-income world suggests the findings might translate beyond the sample studied.

Studies evaluated in this systematic review do not support the claim that the private sector is usually more efficient, accountable, or medically effective than the public sector; however, the public sector appears frequently to lack timeliness and hospitality towards patients.

How the Wealth Gap Damages Democracy

Pacific Standard reviews Inequality and Instability by James K. Galbraith and Affluence & Influence, by Martin Gilen:

Gilens and James K. Galbraith are among the few experts who’ve been working on the subject for more than a decade. Their conclusions reinforce the fears of those of us who’ve suspected that inequality is a blight on American society. Indeed, the damage to democratic values is not in some distant dystopian future: Gilens states plainly that the relationship between the policy desires of the wealthiest 10 percent of the population and actual federal public policy over recent decades “often corresponded more closely to a plutocracy than to a democracy.”

...Galbraith believes that recent volatility in inequality levels stems almost entirely from the increased accumulation of wealth among those working at the top of the technology and finance sectors.

The biggest problem, he insists, is that in recent decades, we seem to have forgotten how to grow the economy except by increasing inequality. The result has been a series of bubbles, and bubbles always cause damage when they pop.

...Gilens’s concerns are different, more pessimistic. He maintains that the poor and middle class have precious little representation in federal policymaking. Surveying a 40-year period, he finds that legislative outcomes almost never correspond to the public opinion preferences of the poor (at least when their expressed interests differ from those of the rich), whereas they much more frequently match the policy preferences of the wealthiest 10 percent. He does not flinch from the harsh conclusion: “The complete lack of government responsiveness to the preferences of the poor is disturbing and seems consistent only with the most cynical views of American politics.”I haven't read either book yet but both sound worth reading.

Congress left our embassies exposed

Salon explores how tax policy decisions contributed to under-protected U.S. embassies:

More discussion at the link.

Among the worst trends in U.S. foreign-policy making in recent decades is the decline of the State Department and the corresponding rise of the Defense Department. State is responsible for American diplomacy — the hard work of negotiating and maintaining relations with other countries; Defense (formerly the Department of War, a more honest designation) looks after war-making and protecting national security. Few things reflect America’s skewed foreign-policy priorities more than the funding discrepancies between the two departments. Consider the numbers:

- ...The State Department’s funding request for 2013 was $51.6 billion, $300 million less than 2012, because, it said, “this is a time of fiscal restraint.”

- The Pentagon’s 2012 budget? $614 billion. Mitt Romney promises to increase defense spending dramatically.

More discussion at the link.

Monday, September 17, 2012

More on those charter cities/ultimate gated communities

Peter Spiro notes that "appeals from courts in the cities would be to Mauritius and then to the UK Privy Council... This strikes me as the leading edge of a potentially huge development, in which private actors more formally get their own pieces of turf and the lines between sovereign entities further blur. ... it will require legal innovation to situate the new, private city-state in the world of international law."

I still think this is just a new twist on an old idea. But I agree that there are serious implications for thinking about the nation state, sovereignty, autonomy, and the rule of law.

I still think this is just a new twist on an old idea. But I agree that there are serious implications for thinking about the nation state, sovereignty, autonomy, and the rule of law.

Which Americans have no health insurance?

The Census has published Income, Poverty and Health Insurance Coverage in the United States: 2011, which yields the following picture of where the 48.6 million Americans without health insurance live (numbers in thousands):

So almost half live in the south, most of which are red states (opposed to national health care, writ large):

So almost half live in the south, most of which are red states (opposed to national health care, writ large):

Summary of results of the 1996, 2000, 2004, and 2008presidential elections:

Many (but not all) spend the least on health care:

And they are among the states with the worst health outcomes across the nation:

States carried by the Republican in all four elections

States carried by the Republican in three of the four elections

States carried by each party twice in the four elections

States carried by the Democrat in three of the four elections

States carried by the Democrat in all four elections

Source: Wikipedia

They are also many of the poorest states:

Source: The Poorest States of America

Many (but not all) spend the least on health care:

And they are among the states with the worst health outcomes across the nation:

Source: What Our Health Spending Buys Us

U.S., U.K. sign FATCA pact

The WSJ blog reports that the U.K. is the first country to agree to implement the tax-reporting requirements under FATCA:

Treasury said it expects to sign agreements with other countries in the near future, noting the U.K. deal is based on a model agreement developed in consultation not just with London but the governments of France, Germany, Italy and Spain.

“We are pleased that the United Kingdom, one of our closest allies, is the first jurisdiction to sign a bilateral agreement with us and we look forward to quickly concluding agreements based on this model with other jurisdictions,” said Mark Mazur, assistant Treasury secretary for tax policy, in a statement.

...While the U.K. agreement is reciprocal, allowing for the sharing of information on U.K. residents held in U.S. financial institutions, other deals may not allow for such exchanges.It's not clear what's in it for the other country if an agreement does not provide for reciprocity; indeed, at least a superficial reciprocity is in general fundamental in the whole history of international tax agreements and I would like to know on what grounds a nonreciprocal agreement would even be contemplated. Why would another country agree to share info with the U.S., to benefit the U.S. alone? This is hardly a model for global tax cooperation, OECD praise notwithstanding. Also each time I see another article about agreements on FATCA, regardless of the substantive content or likely efficacy thereof, the silence between the U.S. and Canada on this issue looms larger.

Friday, September 14, 2012

What is the middle class?

Apropos of this, Jason Myers asks, " If I referred to the middle of my car as every part of it except for the front and rear bumpers, would I have something in mind other than obfuscation or misdirection?"

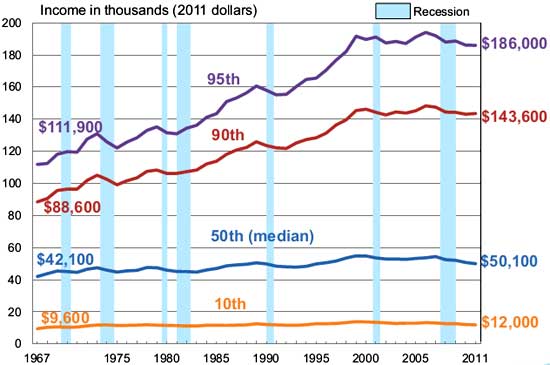

Here is one picture of incomes in America, in case anyone has lost track:

Here is one picture of incomes in America, in case anyone has lost track:

from the Economic Populist, more at the link.

Wednesday, September 12, 2012

Moving McJobs-ward: more jobs but smaller paychecks, plus stagnation in pay equity

There's always plenty of talk about how many jobs have been saved or created but not nearly enough of what kind of jobs there are. That's because quantity is relatively much easier to articulate than quantity and by articulate I mean "use for political purposes." But today, NPR has this:

and this:

and this:

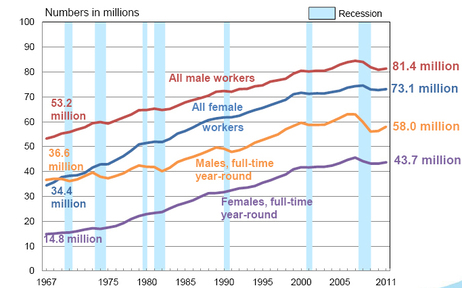

NPR says nothing about the gender pay gap, but isn't it amazing that since...oh, somewhere in the late 80s I guess (the graph inexplicably has no bottom axis but indicates it covers 1967-2011, but the tick marks don't seem to add up right), the two lines stop slowly coming together as they had been, and start moving up and down in sync, apparently perfectly preserving the inequality?

NPR says nothing about the gender pay gap, but isn't it amazing that since...oh, somewhere in the late 80s I guess (the graph inexplicably has no bottom axis but indicates it covers 1967-2011, but the tick marks don't seem to add up right), the two lines stop slowly coming together as they had been, and start moving up and down in sync, apparently perfectly preserving the inequality?

Also for the top chart, I note that of all male workers, 71% are currently in full time jobs now, versus 68% in 1967, while for female workers about 60% are currently full time, versus 43% in 1967.

NPR's point is that "while high unemployment remains a big problem for the U.S. labor market, it's not the only problem. There's also a long-term stagnation in real earnings for people who have jobs."

Moreover one full time job with middle class wages, sick pay, vacation pay, health care benefits, and a pension plan is not equal to one part time job at minimum wage with no benefits of any kind. And the trend is indeed McJobs-ward. Yet the raw number is the primary message of the monthly obsession over job creation/savings.

Also for the top chart, I note that of all male workers, 71% are currently in full time jobs now, versus 68% in 1967, while for female workers about 60% are currently full time, versus 43% in 1967.

NPR's point is that "while high unemployment remains a big problem for the U.S. labor market, it's not the only problem. There's also a long-term stagnation in real earnings for people who have jobs."

Moreover one full time job with middle class wages, sick pay, vacation pay, health care benefits, and a pension plan is not equal to one part time job at minimum wage with no benefits of any kind. And the trend is indeed McJobs-ward. Yet the raw number is the primary message of the monthly obsession over job creation/savings.

Tuesday, September 11, 2012

McGill Tax Policy Colloquium

This fall

marks the third instalment of the McGill University Faculty of Law Tax Policy Colloquium. This year’s colloquium features a number of

distinguished invited speakers who will contribute a rich variety of scholarly

works in progress on topics of national and international tax law and policy

issues. If you will be in Montreal on any of these dates, I invite you to join the tax

policy class to hear presentations by this illustrious group. All presentations begin at 11:35 in New

Chancellor Day Hall, Room 201, at the Faculty of Law, 3644 Rue Peel, Montreal, Quebec.

- Wednesday, Sept. 26: Prof. Miranda Stewart, University of Melbourne Law School

- Monday, Oct. 15: Prof. Arthur Cockfield, Queen’s University Faculty of Law

- Monday, Oct. 29, Prof. Reuven Avi-Yonah, Irwin I. Cohn Professor of Law, University of Michigan School of Law

- Monday, Nov. 5, Prof. Lisa Philipps, York University, Osgoode Hall Law School

- Monday, Nov. 12, Prof. Alain Deneault, Université du Québec a Montréal, Dept. of Sociology

- Monday, Nov. 19, Prof. Colin Campbell, University of Western Ontario Law School

It's déjà vu all over again: constructive receipt edition

William F. Hartman et ux. v. United States; No. 2011-5110

WILLIAM F. HARTMAN AND THERESE HARTMAN,

Plaintiffs-Appellants,

v.

UNITED STATES,

Defendant-Appellee.

UNITED STATES COURT OF APPEALS

FOR THE FEDERAL CIRCUIT

Appeal from the United States Court of Federal Claims

in case no. 05-CV-675, Judge Margaret M. Sweeney.

Decided: September 10, 2012

KENNETH R. BOIARSKY, Kenneth R. Boiarsky, P.C., of El Prado, New Mexico, argued for plaintiff-appellant.

FRANCESCA U. TAMAMI, Attorney, Commercial Litigation Branch, Civil Division, United States Department of Justice, of Washington, DC, argued for defendant-appellee. With her on the brief were TAMARA W. ASHFORD, Deputy Assistant Attorney General, GILBERT S. ROTHENBERG, and KENNETH L. GREENE, Attorneys.

Before DYK, O'MALLEY, and REYNA, Circuit Judges.

DYK, Circuit Judge.

William F. Hartman and Therese Hartman (collectively, "the Hartmans") appeal a decision of the United States Court of Federal Claims ("Claims Court") granting summary judgment to the government on the Hartmans' claim for a federal income tax refund. Hartman v. United States, 99 Fed. Cl. 168 (2011). Because the Claims Court properly determined that the Hartmans were not entitled to a refund, we affirm.

BACKGROUND

This case requires an interpretation of the Treasury Regulations governing the constructive receipt of income, which in turn interprets section 451 of the Internal Revenue Code, imposing a tax on "[t]he amount of any item of gross income . . . for the taxable year in which received by the taxpayer."1 I.R.C. § 451(a). Under the Treasury Regulations, taxpayers computing their taxable income under the cash receipts and disbursements method must include as taxable income "all items which constitute gross income . . . for the taxable year in which actually or constructively received." Treas. Reg. § 1.446-1(c)(i). "Income . . . is constructively received by [a taxpayer] in the taxable year during which it is credited to his account, set apart for him, or otherwise made available so that he may draw upon it at any time, or so that he could have drawn upon it during the taxable year if notice of intention to withdraw had been given. However, income is not constructively received if the taxpayer's control of its receipt is subject to substantial limitations or restrictions." Id. § 1.451-2(a).

The question here is whether Mr. Hartman constructively received all shares of stock allocated to him for the sale of Ernst & Young LLP's ("E&Y") consulting business in 2000 (as originally reported) or whether he received only that portion of the shares which had been monetized (sold) in 2000 (as reflected in the Hartmans' amended return and request for a refund).2

I

The background of this dispute began in 1999. In late 1999, E&Y was preparing to sell its consulting business to Cap Gemini, S.A. ("Cap Gemini"), a French corporation. At this time, Mr. Hartman was an accredited consulting partner of E&Y. On February 28, 2000, E&Y and Cap Gemini devised a Master Agreement for the sale of E&Y's consulting business. Under the Master Agreement, E&Y would form a new entity, Cap Gemini Ernst & Young U.S. LLC ("CGE&Y"), and would then transfer E&Y's consulting business to CGE&Y in exchange for interest in CGE&Y. Each accredited consulting partner in E&Y, including Mr. Hartman, would then receive a proportionate interest in CGE&Y. Each partner would terminate his partnership in E&Y, retaining his interest in CGE&Y. The accredited consulting partners would then transfer all of their interests in CGE&Y to Cap Gemini. In exchange for their respective interests in CGE&Y, E&Y and the accredited consulting partners were to receive shares of Cap Gemini common stock. The shares of Cap Gemini common stock would be allocated to each accredited consulting partner in accordance with his proportionate interest in CGE&Y. Additionally, each accredited consulting partner was to sign an employment contract with CGE&Y, which would include a non-compete provision. CGE&Y would then become the entity through which Cap Gemini would conduct its consulting business in North America.

As a part of the transaction described in the Master Agreement, each accredited consulting partner was also required to execute and sign a Consulting Partner Transaction Agreement ("Partner Agreement") between the partners, E&Y, Cap Gemini, and CGE&Y. Under the Partner Agreement, the Cap Gemini shares received by each accredited consulting partner would be placed into separate Merrill Lynch restricted accounts in each individual partner's name. The Partner Agreement further provided that for a period of four years and 300 days following the closing of the transaction, the accredited consulting partners could not "directly or indirectly, sell, assign, transfer, pledge, grant any option with respect to or otherwise dispose of any interest" in the Cap Gemini common stock in their restricted accounts, except for a series of scheduled offerings as set forth in a separate Global Shareholders Agreement ("Shareholders Agreement"). J.A. B-627. The Shareholders Agreement provided for an initial sale of 25% of the shares held by each accredited consulting partner in order to satisfy each partner's tax liability in the year 2000 as a result of the transaction, and subsequent offerings of varying percentages at each anniversary following closing.3 Although their right to sell or otherwise dispose of Cap Gemini shares was restricted, the accredited consulting partners enjoyed dividend rights on the Cap Gemini shares beginning on January 1, 2000, without restriction. The dividends earned on the Cap Gemini shares were not subject to forfeiture. Additionally, the accredited consulting partners had voting rights on the Cap Gemini shares held in the restricted accounts, though they provided powers of attorney to the CEO of CGE&Y to vote the shares on their behalf.

In addition to the restrictions on the sale of the shares, certain percentages ("forfeiture percentages") of the Cap Gemini shares were subject to forfeiture "as liquidated damages." J.A. B-628. The percentage of shares subject to forfeiture declined over the life of the agreement and expired entirely at four years and 300 days following closing.4 In the period four years and 300 days following closing, the applicable forfeiture percentages of the shares would be forfeited if the accredited consulting partner (1) breached his employment contract with CGE&Y; (2) left CGE&Y voluntarily; or (3) was terminated for cause. Id. Additionally, where the accredited consulting partner was terminated for "poor performance," he would forfeit at least fifty percent of the applicable forfeiture percentage.5 Notwithstanding the monetization restrictions and forfeiture provisions, the Master Agreement provided that the parties, including the accredited consulting partners, "agree that for all US federal . . . Tax purposes the transactions undertaken pursuant to [the Master] Agreement will be treated and reported by them as . . . a sale of a portion of the [CGE&Y] interests by . . . the Accredited Partners to [Cap Gemini] in exchange for the Ordinary Shares [of Cap Gemini]."6 J.A. B-123-24. Cap Gemini was required to provide E&Y and each accredited consulting partner with a Form 1099-B with respect to its acquisition of the CGE&Y interests.7 The Master Agreement also provided that "the parties agree that all [Cap Gemini] Ordinary Shares that are not monetized in the Initial Offering will be valued for tax purposes at 95% of the otherwise-applicable market price." J.A. B-555.

II

In early March of 2000, E&Y held a meeting in Atlanta with all E&Y partners to discuss the details of the proposed transaction with Cap Gemini. Prior to the meeting, E&Y distributed a Partner Information Document, dated March 1, 2000, to its partners which summarized the Master Agreement and Partner Agreement, and purported to explain the tax consequences of the transaction as set forth in those agreements. The Partner Information Document provided that "[t]he sale of Consulting Services to Cap Gemini is a taxable capital gains transaction," and that the partners would be "responsible for paying [their] own taxes out of the proceeds allocated to [them]; however, [each would] receive funds from the sale of Cap Gemini shares for [their] tax obligations as they come due." J.A. B-726. The document further provided that "[t]he gain on the sale of the distributed [CGE&Y] shares is reportable on Schedule D of [each partner's] U.S. federal income tax return for 2000." J.A. B-727.

Mr. Hartman and the other E&Y accredited consulting partners signed the Partner Agreement prior to May 1, 2000, and the transaction closed on May 23, 2000. By signing the Partner Agreement, Mr. Hartman became a party to the Master Agreement and thereby "agree[d] not to take any position in any Tax Return contrary to the [Master Agreement] without the written consent of [Cap Gemini]." J.A. B-124. Mr. Hartman received 55,000 total shares of Cap Gemini common stock, which were deposited into his restricted account. Twenty-five percent of Mr. Hartman's Cap Gemini shares (necessary for payment of income taxes related to the transaction) were sold in May of 2000 for approximately 158 Euros per share, for a total monetization of $2,179,187 in U.S. dollars, which was deposited into Mr. Hartman's restricted account.

On February 26, 2001, Mr. Hartman received a Form 1099-B from Cap Gemini reflecting the consideration he was deemed to have received under the Master Agreement (a total value of $8,262,183), including a valuation of his unsold Cap Gemini shares at approximately $148 per share (reflecting 95% of the market value of the shares). On August 8, 2001, the Hartmans filed a joint federal income tax return for 2000, reporting the entire amount listed on the Form 1099-B (less cost or other basis) as capital gains income. Additionally, in filing its own 2000 federal tax return, Cap Gemini used the 95% valuation of the shares to determine the value of intangible assets to be amortized pursuant to I.R.C. § 197.8

III

Following closing of the transaction, the value of Cap Gemini shares dropped drastically, from approximately $155 per share at closing to $56 per share by October 2001. Mr. Hartman voluntarily terminated his employment with CGE&Y on December 31, 2001.9 Upon his departure, Mr. Hartman forfeited 10,560 shares of his Cap Gemini stock and received a credit for the taxes he paid on those shares in his 2000 tax return pursuant to I.R.C. § 1341, which provides for the computation of tax where a taxpayer restores amounts previously held under a claim of right. In December 2003, the Hartmans filed an amended federal tax return for 2000, claiming that they had received only the 25% of Cap Gemini shares that had been monetized in the year 2000, with the remainder being received in 2001 and 2002. They sought a refund of $1,298,134. The Internal Revenue Service ("IRS") failed to act on the Hartmans' claim for a refund, and on June 21, 2005, the Hartmans filed suit in the Claims Court against the government seeking a refund of taxes paid for 2000.

The Claims Court found that the Hartmans had constructively received all 55,000 shares of Cap Gemini common stock in 2000, and that the Hartmans had properly reported the gain from the transaction on their income tax return for 2000 and thus were not entitled to a tax refund. Accordingly, the court granted summary judgment for the government, and the Hartmans timely appealed. We have jurisdiction pursuant to 28 U.S.C. § 1295(a)(3). We review "the summary judgment of the Court of Federal Claims, as well as its interpretation and application of the governing law, de novo." Gump v. United States, 86 F.3d 1126, 1127 (Fed. Cir. 1996).

DISCUSSION

I

The Hartmans' claim for a refund of taxes paid based on the transaction at issue in this case is not unique. Three courts of appeals have already squarely addressed the issue presented before us with respect to other similarly situated former E&Y accredited consulting partners. Each circuit to consider the transaction at issue here has concluded that the taxpayers were not entitled to a refund of taxes paid in 2000. See United States v. Fort, 638 F.3d 1334 (11th Cir. 2011); United States v. Bergbauer, 602 F.3d 569 (4th Cir. 2010); United States v. Fletcher, 562 F.3d 839 (7th Cir. 2009).10 As it argued before the Claims Court and the Fourth, Seventh, and Eleventh Circuits, the government contends that the Hartmans are not entitled to a tax refund for two reasons.

First, the government argues that under the "Danielson Rule," the Hartmans may not disavow receipt of the Cap Gemini shares in 2000 after having agreed to be bound by the Master Agreement which required them to recognize the shares as received in 2000 for the purposes of their federal income tax returns. The "Danielson Rule" takes its name from Commissioner v. Danielson, 378 F.2d 771 (3d Cir. 1967) (en banc), cert. denied, 389 U.S. 858 (1967), where the rule was described:

[A] party can challenge the tax consequences of his agreement as construed by the Commissioner [of Internal Revenue] only by adducing proof which in an action between the parties to the agreement would be admissible to alter that construction or to show its unenforceability because of mistake, undue influence, fraud, duress, etc.

Id. at 775. Our predecessor court expressly adopted the Danielson Rule, see Proulx v. United States, 594 F.2d 832, 839-42 (Ct. Cl. 1979); Dakan v. United States, 492 F.2d 1192, 1198-1200 (Ct. Cl. 1974), and we have consistently applied the rule in subsequent cases involving "stock repurchase agreements which contain express allocations of monetary consideration between stock and non-stock items," Lane Bryant, Inc. v. United States, 35 F.3d 1570, 1575 (Fed. Cir. 1994); see Stokely-Van Camp, Inc. v. United States, 974 F.2d 1319, 1325-26 (Fed. Cir. 1992).11

Here, the government seeks to extend the Danielson Rule to situations where the taxpayer agrees, not to the allocation of consideration, but to a particular tax treatment for the consideration, i.e., when the consideration is received by the taxpayer. Although the Claims Court recognized the Danielson Rule as "binding" in this circuit, it concluded that the rule is limited only to situations where "a taxpayer challenges express allocations of monetary consideration," rather than a situation where, as in this case, a taxpayer challenges how a transaction should be treated for tax purposes, and refused to apply the rule. Hartman, 99 Fed. Cl. at 181-82 (internal quotation mark omitted). In this appeal, it appeared that the parties differed as to whether the Hartmans were obligated under an agreement with Cap Gemini to report the shares of Cap Gemini stock as received in 2000, and we requested and received supplemental briefing on that issue.

Second, the government contends that, although the shares were not actually received in 2000, Mr. Hartman nonetheless constructively received the shares in accordance with Treas. Reg. § 1.451-2. In addressing this issue, the Claims Court noted that "while the shares were held in the restricted account, Mr. Hartman could vote them and receive dividends from them," and therefore, "Mr. Hartman received all of the shares, for tax purposes, in 2000, when they were issued to him by Cap Gemini." Hartman, 99 Fed. Cl. at 187. The court further reasoned that "[t]he control that Mr. Hartman exercised over his Cap Gemini stock in 2000 was not defeated by the monetization restrictions and forfeiture conditions described in the transaction documents," because "Mr. Hartman voluntarily agreed to accept his share of the transaction proceeds with these limitations." Id. at 185. Thus, the Claims Court concluded that the shares of Cap Gemini stock were constructively received by Mr. Hartman in 2000.

Because we agree that Mr. Hartman "constructively received" the Cap Gemini shares in 2000 under the Treasury Regulations, we need not reach the questions of whether the agreements did in fact require the Hartmans to report the shares as received in 2000, and if so, whether the Danielson Rule could apply to situations where parties agree to a particular tax treatment.

II

The constructive receipt issue turns on the interpretation of the constructive receipt regulation, Treas. Reg. § 1.451-2, and whether, under that regulation, Mr. Hartman constructively received all of his allocated shares of Cap Gemini stock in 2000.

We note initially that although the accredited consulting partners' right to "sell, assign, transfer, pledge, grant any option with respect to or otherwise dispose of any interest" in the Cap Gemini common stock was restricted, the Cap Gemini shares here were set aside for each accredited consulting partner in a Merrill Lynch account in each partner's name, and the partners were able to receive dividends from and vote the shares (though subject to a power of attorney) during the period of time in which the sale of the shares was restricted. The risk of a decline in the value of the shares and the benefits of any increase in the value of the shares accrued entirely to the accredited consulting partners. Under the agreement, the shares immediately vested in the partners to ensure that the shares would not be treated as deferred compensation for future services.12 Thus, the benefit of ownership of the Cap Gemini stock to each accredited consulting partner extended far beyond "the mere crediting [of the stock] on the books of the corporation."13

It appears that the Hartmans make three arguments with respect section 1.451-2 of the Treasury Regulations. First, relying on the "or otherwise made available so that he may draw upon it at any time" language in the regulation, the Hartmans contend that the Cap Gemini shares were not constructively received when placed into Mr. Hartman's restricted account because he could not access them under the provisions of the Partner Agreement. But, as the government points out, constructive receipt extends to many situations in which the taxpayer cannot immediately draw upon the account. The quintessential example of constructive receipt covers the situation in which a taxpayer cannot, by his own agreement, presently receive an asset. See Goldsmith v. United States, 586 F.2d 810, 815 (Ct. Cl. 1978) ("[U]nder the doctrine of constructive receipt a taxpayer may not deliberately turn his back upon income and thereby select the year for which he will report it.").

Second, the Hartmans argue alternatively that at the time that Mr. Hartman entered into the Partner Agreement, he was not presented with the alternative option of receiving the assets free of restriction. But as discussed below, the existence of an opportunity to receive the assets at the time of escrow creation, i.e., free of all restrictions, is not a necessary requirement for constructive receipt. There is constructive receipt if the taxpayer exercised substantial control over the escrow account. Finally, the Hartmans urge that even if they are wrong as to their first two arguments, the accredited consulting partners did not have sufficient control over the shares to constitute constructive receipt. Relying on section 1.451-2 of the Treasury Regulations and our interpretation of that regulation in Patton v. United States, 726 F.2d 1574 (Fed. Cir. 1984), the Hartmans contend that Patton held that there is no constructive receipt where a third party controls the right to receive the shares (or certificates). This last argument warrants some discussion.

In Patton, a subchapter S corporation determined to make a $346,000 distribution to its shareholders.14 Because of its insolvency, the corporation was unable to make the distribution to the shareholders from its own funds and had to borrow the $346,000 to distribute to its shareholders. Id. at 1575-76. The corporation secured a loan from the bank and then purchased three certificates of deposit in the names of its shareholders (two for $115,000 and one for $116,000). Id. at 1576. The IRS claimed that the certificates represented dividend income to the shareholders in 1974, the tax year of the purchase of the certificates of deposit. The taxpayers claimed that the dividends would not be received until the certificates matured (upon the corporation's repayment of the $346,000 loan to the bank). The two $115,000 certificates were pledged as collateral for the loan, and thus "were never set aside for the individual benefit of the shareholders, but remained in the custody and control of the bank as collateral," and could not "have [been] delivered . . . to the shareholders had they so demanded." Id. (internal quotation marks omitted). The third certificate was made payable to the shareholders such that they could pay their federal income taxes on the distributed income. Id. On its federal income tax return for the year in which the certificates were purchased, the corporation reported that all the income had been distributed, while the shareholders failed to report receipt of any of the certificates as taxable income. Id.

We held that, while the third certificate was income to the shareholders, the two pledged certificates of deposit were not "constructively received" by the shareholders, reasoning:

Although the [shareholders] may have become the owners of the [pledged] certificates of deposit when the bank issued the certificates . . . in the name of the [shareholders] . . . , at that time the certificates were not "unqualifiedly made subject to their demands" and the [shareholders] did not constructively receive them. . . . The [shareholders] did not constructively receive the certificates because, except for the receipt of the interest from the certificates, the [shareholders] could not have obtained or directed the distribution of the certificates.

Id. at 1577. We further noted that "it was far from certain that the [shareholders] ever would obtain the certificates, since the corporation's financial condition might result in its default on the loan and the bank's consequent foreclosure of the pledge of the certificates," id., and "[t]he control and authority of the bank over the certificates of deposit . . . constituted 'substantial limitations or restrictions' upon the appellants' control over receipt of the certificates," id. at 1578.

The Hartmans contend that, as in Patton, Mr. Hartman did not constructively receive the shares of Cap Gemini stock in 2000 (except for those shares that were monetized) because his receipt of the shares was subject to "substantial limitations or restrictions," i.e., the distribution of the shares was within the control of a third party.

However, the Hartmans' reliance on Patton is misplaced. Two significant features distinguish this case from Patton. First the restrictions were imposed by the taxpayer's own agreement and not by an agreement between the distributing corporation and a third party (the bank in Patton). Unlike Patton, Mr. Hartman and the other accredited consulting partners agreed to condition receipt of their shares on satisfaction of their own contractual obligations under the Partner Agreement and their employment contracts with CGE&Y. Under such circumstances, Mr. Hartman cannot now be heard to complain that such restrictions undermine his constructive receipt of the shares. The Claims Court rightly found that "Mr. Hartman voluntarily agreed to accept his share of the transaction proceeds with these limitations." Hartman, 99 Fed. Cl. at 185. The fact that Mr. Hartman voluntarily agreed to subject himself to the restrictions imposed by the Partner Agreement cannot defeat constructive receipt. See Soreng v. Comm'r, 158 F.2d 340, 341 (7th Cir. 1947) ("We can discern no rational basis for a holding that the dividends received by the [taxpayers] are not includable in gross income merely because they or [sic] their own accord entered into a contract with a third party as to the manner of their disposition when received."). As the Fourth Circuit in Harris v. Commissioner, 477 F.2d 812, 817 (4th Cir. 1973), noted when interpreting section 1.451-2 of the Treasury Regulations, "[s]ale proceeds, or other income, are constructively received when available without restriction at the taxpayer's command; the fact that the taxpayer has arranged to have the sale proceeds paid to a third party and that the third party is, with taxpayer's agreement, not legally obligated to pay them to taxpayer until a later date, is immaterial."

Second, under the Partner Agreement, the conditions that could result in forfeiture were within the control of the accredited consulting partners themselves rather than within the control of Cap Gemini. In Patton, the shareholders had no control over their receipt of the certificates, and indeed may have never received them, due only to the corporation's failure to comply with its obligations to the bank, not due to any obligations of their own. Here, each partner had direct control over whether the shares would later be forfeitable. See Fort, 638 F.3d at 1341. The forfeited shares were characterized in the agreement as "liquidated damages," and were forfeitable only where partner breached his employment contract, left CGE&Y voluntarily, or was terminated for cause or poor performance, all circumstances over which the accredited consulting partners exercised control. See J.A. B-628.

Although the Hartmans contend that the determination of "poor performance" was within the control of Cap Gemini, the Hartmans have pointed to no evidence in the record to suggest that the "poor performance" clause could be utilized to terminate employees due to circumstances outside of the employees' control.15 As the Eleventh Circuit recently noted, "the plain meaning of being terminated for 'poor performance' is not being terminated for any reason at all. Rather, poor performance clearly refers to unsatisfactory performance. It would be a strained interpretation . . . to hold that 'poor performance' does not really mean poor performance, but actually means 'any reason at all.'" Fort, 638 F.3d at 1342.

Other circuits, even before the Cap Gemini controversy, have held that where restrictions on receipt are imposed in order to guarantee performance under a contract, the income is nonetheless received when set aside for the taxpayer. See Chaplin v. Comm'r, 136 F.2d 298, 301-02 (9th Cir. 1943); Bonham v. Comm'r, 89 F.2d 725, 727-28 (8th Cir. 1937).16

In Chaplin, Chaplin, an artist, received two certificates of stock (167 shares each) in United Artists Corporation ("United") in 1928; however the certificates were immediately placed in escrow until 1935. 136 F.2d at 299. Under the terms of an agreement between Chaplin and United, Chaplin was required to deliver five motion picture photoplays to United. Id. at 301. Upon delivery of each photoplay, one fifth of the shares held in escrow were to be released to Chaplin. Id. The Ninth Circuit held that the United shares had been received by Chaplin when they were placed into escrow. Specifically, the court reasoned that "[o]ne nonetheless owns personal property because held by another to insure the performance of a contract." Id. at 302. Similarly, in Bonham, the Eighth Circuit held that where "stock was issued, the title passed then to [taxpayer], and the stock was retained as a pledge" to guarantee performance, the shares were taxable in the year that title passed to the taxpayer. 89 F.2d at 727.

The Hartmans contend that Chaplin and Bonham are inapplicable here because those cases were decided before the adoption of the constructive receipt regulation at issue here. See Republication of Regulations, 25 Fed. Reg. 11,402, 11,710 (Nov. 26, 1960) (to be codified at 26 C.F.R. pt. 1). However, nothing in the regulatory history of section 1.451-2 indicates that the IRS intended to overrule the holdings of Chaplin and Bonham, and indeed, Chaplin and Bonham are consistent with the regulation. Notably, the IRS General Counsel Memorandum, issued after adoption of the constructive receipt regulation, cited Chaplin and Bonham with approval, noting that where "the taxpayer exercises a considerable degree of domination and control over the assets in escrow, the courts and the Service have generally held . . . that income is presently realized notwithstanding that the taxpayer lacks an absolute right to possess the escrowed assets." See I.R.S. Gen. Couns. Mem. 37,073 (Mar. 31, 1977). The language of the regulation is consistent with those cases, providing that "income is not constructively received if the taxpayer's control of its receipt is subject to substantial limitations or restrictions," i.e. that the "control" over receipt lies with a third party and not with the taxpayer. Treas. Reg. § 1.451-2(a) (emphasis added). In both Chaplin and Bonham, it was the taxpayer's conduct that determined whether he would receive the stock at issue, not a decision by a third party. The stock in Chaplin and Bonham was to be released to the taxpayer upon fulfillment of his contractual obligation, over which he exercised complete control. See Chaplin, 136 F.2d at 302; Bonham, 89 F.2d at 727-28.

We agree with the Seventh Circuit that here "[t]he sort of contingencies that could lead to forfeitures were within the expartners' control. That implies taxability in 2000, for control is a form of constructive possession." Fletcher, 562 F.3d at 845; see also Fort, 638 F.3d at 1342 ("[C]onstructive receipt was not impossible simply because [taxpayer] was required to forfeit the shares upon the occurrence of certain conditions, because [taxpayer] had sufficient control over whether those conditions would occur."). By agreeing to condition release of the shares on continued employment with the corporation (a contractual obligation, satisfaction of which only he controlled), Mr. Hartman exercised control over his receipt of the shares.

In summary, under Mr. Hartman's own agreement, the Cap Gemini shares were "set aside" for Mr. Hartman in a brokerage account. Mr. Hartman received dividends from and was entitled to vote the shares in the year 2000. Mr. Hartman exercised control over his receipt of the Cap Gemini shares under the forfeiture provisions of the Partner Agreement. In light of these attributes of dominion and control, we conclude that Mr. Hartman constructively received all 55,000 shares of Cap Gemini common stock in 2000 when they were placed into his restricted account to guarantee his performance under his contractual obligations.

The Claims Court's decision granting summary judgment to the government on the Hartmans' claim for a refund of federal income taxes paid in 2000 is affirmed.

AFFIRMED.

FOOTNOTES

1 See Mayo Found. for Med. Educ. & Research v. United States, 131 S. Ct. 704, 713 (2011) ("The principles underlying our decision in Chevron apply with full force in the tax context. . . . Filling gaps in the Internal Revenue Code plainly requires the Treasury Department to make interpretive choices for statutory implementation at least as complex as the ones other agencies must make in administering their statutes. We see no reason why our review of tax regulations should not be guided by agency expertise pursuant to Chevron to the same extent as our review of other regulations." (citing Chevron, U.S.A., Inc. v. Natural Res. Def. Council, Inc., 467 U.S. 837, 843-44 (1984))).

2 Although the transaction at issue in this case (the sale of E&Y's consulting business to Cap Gemini) involves only Mr. Hartman, both Mr. and Mrs. Hartman filed suit for a refund of taxes paid based on the transaction, as they filed a joint tax return in 2000.

3 The monetization schedule was later modified from annual scheduled offerings to "a more flexible approach that allows one or more transactions over the course of each year." J.A. B-682.

4 The applicable forfeiture percentages were 75% prior to the first anniversary of closing; 56.7% prior to the second anniversary of closing; 38.4% prior to the third anniversary of closing; 20% prior to the fourth anniversary of closing; and 10% prior to the fourth anniversary of closing plus 300 days. At four years and 300 days following closing, the Cap Gemini shares were no longer subject to forfeiture.

5 Where a partner was terminated for "poor performance," a review committee comprised of senior executives selected by CGE&Y would determine an appropriate amount of forfeiture between 50% and 100% of the applicable forfeiture percentage.

6 The Partner Agreement further provided that the accredited consulting partners "acknowledge [their] obligation to treat and report the Transaction for all relevant tax purposes in the manner provided in . . . the Master Agreement." J.A. B-624.

7 IRS Form 1099-B, Proceeds From Broker and Barter Exchange Transactions, is the tax form on which sales or redemptions of securities, futures transactions, commodities, and barter exchange transactions are reported.

8 Cap Gemini was later audited by the IRS, which conducted an examination of the transaction between Cap Gemini and E&Y, but did not make any adjustments to the tax treatment of the transaction.

9 Although Mr. Hartman ceased performing any duties for CGE&Y on December 31, 2001, he was permitted to remain an employee of CGE&Y through May 24, 2002 (following the second anniversary of closing) to allow him to reduce his applicable forfeiture percentage from 56.7% to 38.4%.

10 Several district courts have also reached the same conclusion. See, e.g., United States v. Fort, No. 1:08-CV-3885, 2010 WL 2104671 (N.D. Ga. May 20, 2010), aff'd, 638 F.3d 1334 (11th Cir. 2011); United States v. Nackel, 686 F. Supp. 2d 1008 (C.D. Cal. 2009); United States v. Berry, No. 06N-CV-211, 2008 WL 4526178 (D.N.H. Oct. 2, 2008); United States v. Bergbauer, No. RDB-05R-2132, 2008 WL 3906784 (D. Md. Aug. 18, 2008), aff'd, 602 F.3d 569 (4th Cir. 2010), cert. denied, 131 S. Ct. 297 (2010); United States v. Fletcher, No. 06 C 6056, 2008 WL 162758 (N.D. Ill. Jan. 15, 2008), aff'd, 562 F.3d 839 (7th Cir. 2009); United States v. Culp, No. 3:05-cv-0522, 2006 WL 4061881 (M.D. Tenn. Dec. 29, 2006).

11 For tax purposes, monetary consideration allocated to the purchase of stock is treated differently from monetary consideration allocated to the purchase of non-stock intangibles such as a covenant not to compete. While the amount allocated towards the purchase of stock is taxed as a capital gains transaction, "the amount a buyer pays a seller for [ ] a covenant [not to compete], entered into in connection with a sale of a business, is ordinary income to the covenantor and an amortizable item for the covenantee." Danielson, 378 F.2d at 775.

12 The Hartmans rely on cases where income was placed in escrow or in trust with the understanding that specified amounts would be released to the taxpayer for performance of future services. These cases hold that, where the taxpayer could not elect immediate receipt, the income was not constructively received when placed in escrow. See, e.g., Drysdale v. Comm'r, 277 F.2d 413 (6th Cir. 1960) (compensation paid by employer to trustee to be released to employee upon satisfaction of contractual employment obligations was not constructively received by employee until released). However, in the present case, the Hartmans (understandably) do not contend that the Cap Gemini shares held in the restricted accounts represent payment for Mr. Hartman's services in CGE&Y, since such an arrangement would result in taxation of the shares as ordinary income rather than as capital gains.

13 The constructive receipt regulation states that "if a corporation credits its employees with bonus stock, but the stock is not available to such employees until some future date, the mere crediting on the books of the corporation does not constitute receipt." Treas. Reg. § 1.451-2(a).

14 A "subchapter S corporation" is a small business corporation established under subchapter S of the Internal Revenue Code, I.R.C. §§ 1361-1379, in which "each shareholder is taxed upon his or her share of the corporation's income." Patton, 726 F.2d at 1575.

15 Indeed, testimony presented before the Claims Court indicated that where employees were terminated due to a reduction in force (which was based on business necessity rather than performance), they did not forfeit any shares. See J.A. C-494-95.

16 See also Fort, 638 F.3d at 1339 (citing Chaplin and Bonham); Fletcher, 562 F.3d at 844 (same).

Subscribe to:

Posts (Atom)